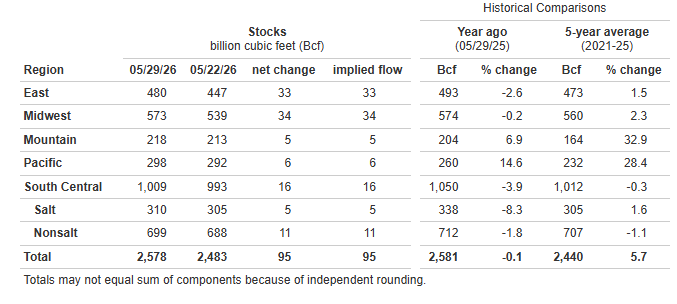

EIA Natural Gas Storage as of 5/29/26, as reported 6/04/26

*Working gas in storage was 2,578 Bcf as of Friday, May 29, 2026, according to EIA estimates. This represents a net increase of 95 Bcf from the previous week. Stocks were 3 Bcf less than last year at this time and 138 Bcf above the five-year average of 2,440 Bcf. At 2,578 Bcf, total working gas is within the five-year historical range.

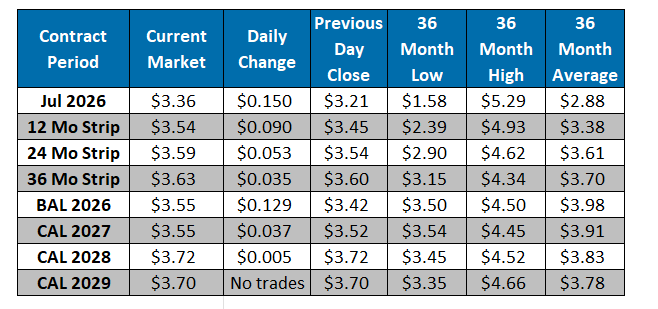

The NYMEX July contract closed at $3.21/MMBtu yesterday, a $0.04/MMBtu increase from Tuesday’s close. This week, July has averaged $3.23/MMBtu, around $0.09/MMBtu above last week’s average of $3.14/MMBtu. It is trading at $3.36/MMBtu, up $0.15/MMBtu from yesterday’s close. Near-term, the market is attempting to stabilize as building heat in Weeks 2 and 3 provides some demand-side support, though the fundamental picture remains mixed. Production continues to struggle, with intraday downward revisions to Permian volumes for the second straight day leaving yesterday’s L48 print at 106.6 Bcf/d and today’s early read only slightly higher at ~107 Bcf/d. Canadian imports are firm at 5.3 Bcf/d on the week. Power demand is picking up as warmer-than-normal weather moves into the Northeast and Midwest, with demand potentially rising more than 25% above current levels by end of next week as the pattern holds. LNG feedgas is 17.52 Bcf/d, with Corpus Christi flows remaining suppressed at 2.48 Bcf/d due to the Sinton compressor station maintenance event expected to last through June 9th — Sabine Pass has rebounded to 4.7 Bcf/d with all engines running at Train 6, partially offsetting the Corpus weakness. Mexican pipeline exports are steady at 7.3 Bcf/d on the week.

*Source: U.S. Energy Information Administration (EIA) Weekly Natural Gas Storage Report

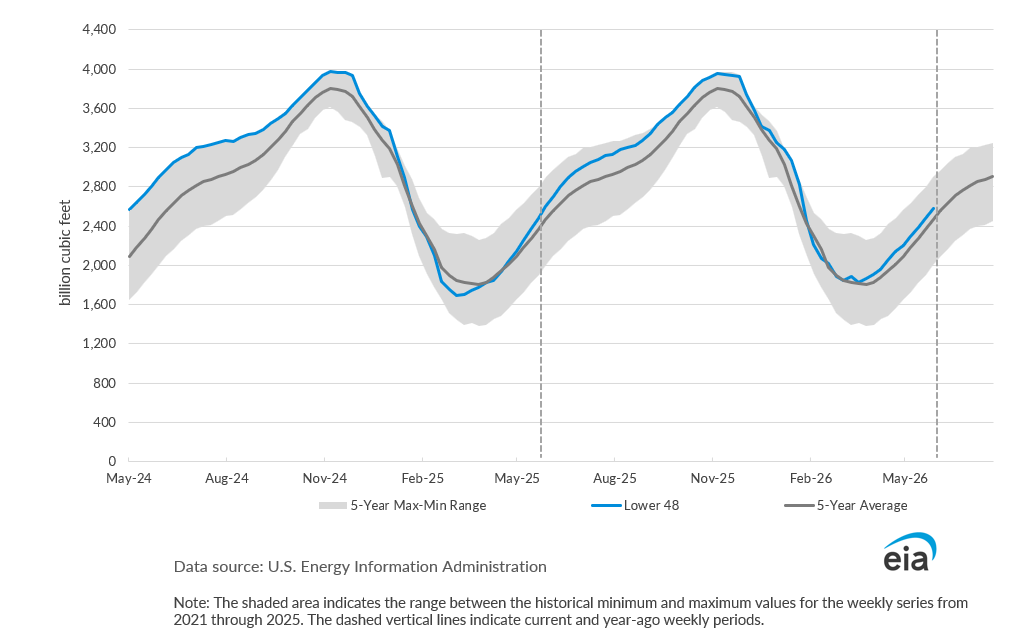

Working Gas in Underground Storage, Lower 48

Working Gas in Underground Storage vs. 5-Year Maximum and Minimum

Current Market