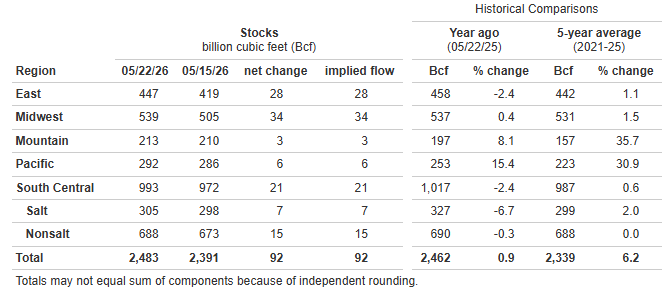

EIA Natural Gas Storage as of 5/22/26, as reported 5/28/26

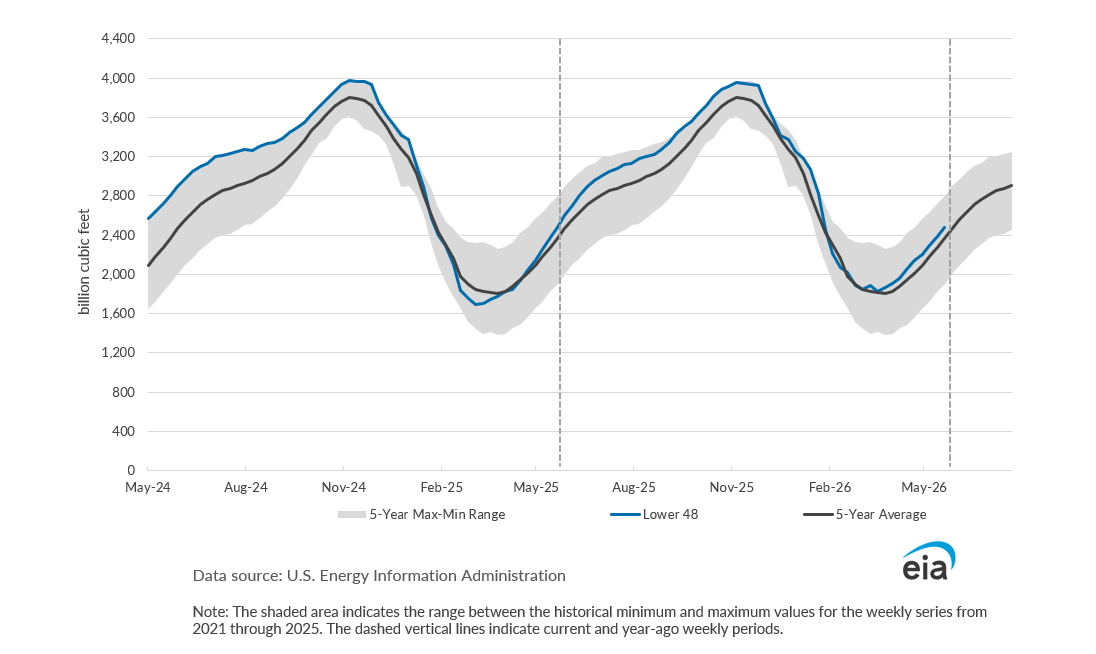

*Working gas in storage was 2,483 Bcf as of Friday, May 22, 2026, according to EIA estimates. This represents a net increase of 92 Bcf from the previous week. Stocks were 21 Bcf higher than last year at this time and 144 Bcf above the five-year average of 2,339 Bcf. At 2,483 Bcf, total working gas is within the five-year historical range.

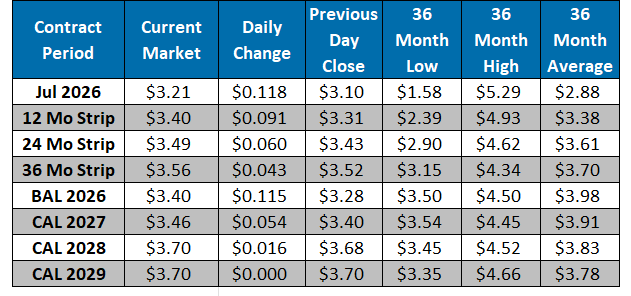

The NYMEX July contract closed at $3.09/MMBtu yesterday, a $0.85/MMBtu increase from Tuesday’s close. This week, July has averaged $3.08/MMBtu, around $0.10/MMBtu below last week’s average of $3.18/MMBtu. It is trading at $3.21/MMBtu, up $0.11/MMBtu from yesterday’s close. Near-term, the market is searching for direction as July takes over as the front-month, with a modest technical reset higher following June’s final settlement at $3.040 doing little to resolve the underlying fundamental picture. Production has pulled back to ~107 Bcf/d, Permian volumes under pressure as a couple of producers have reported price-related shut-ins in the basin, though the expected in-service of the 0.57 Bcf/d GCX expansion in Q2 should help incentivize a recovery. Power burns remain strong as warmer than normal weather lingers across the NE and MW, though a cooler pattern building in the East over the next few days could weigh on near-term gas demand. LNG feedgas is 18.66 Bcf/d, with Corpus Christi flows hitting a new high at 3.794 Bcf/d today and the final mid-scale Stage 3 train expected online later this summer, though a pigging event on Creole Trail May 31-June 1 will likely cut Sabine Pass deliveries by ~0.8 Bcf/d on those days. Mexican pipeline exports are firm at 7.4 Bcf/d on the week.

*Source: U.S. Energy Information Administration (EIA) Weekly Natural Gas Storage Report

Working Gas in Underground Storage, Lower 48

Working Gas in Underground Storage vs. 5-Year Maximum and Minimum

Current Market