ERCOT has requested a waiver from the Public Utility Commission of Texas (PUCT) to skip publishing its May 2026 Capacity, Demand, and Reserves (CDR) report due to ongoing changes to its Long-Term Load Forecast (LTLF) methodology. Because the load forecast is a key input to the CDR and may not be finalized until mid-August 2026, ERCOT argued that releasing a delayed CDR later in the year would provide limited value, especially with the December 2026 CDR scheduled shortly thereafter.

The underlying issue stems from ERCOT’s 2026 Preliminary Long-Term Load Forecast, which projects unprecedented demand growth driven largely by large-load customers. The forecast estimates peak demand reaching 278 GW by 2029 and nearly 368 GW by 2032. ERCOT expressed concerns that these figures may overstate near-term demand due to supply chain limitations and uncertainties surrounding the timing of large-load projects coming online.

To address these concerns, ERCOT has proposed adjusting the forecast using one of two methodologies: a historical realization-rate approach based on actual large-load energization success rates, or a “Batch Zero” forecast approach specifically designed to evaluate the likelihood of large-load projects materializing. ERCOT has recommended the Batch Zero option, arguing it provides a more realistic and actionable foundation for transmission planning, resource adequacy assessments, and the 2026 Triennial Reliability Assessment.

For market participants, the filing highlights ERCOT’s effort to balance planning for rapid load growth while avoiding overbuilding infrastructure based on speculative demand projections. The outcome of the PUCT’s decision on the forecast adjustment methodology will significantly influence future transmission development plans, reliability studies, and long-term resource planning across the ERCOT market.

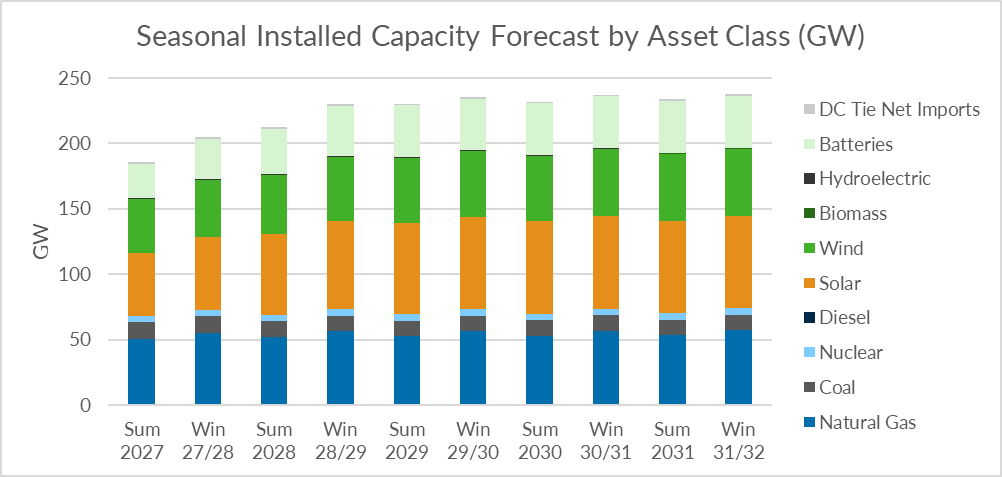

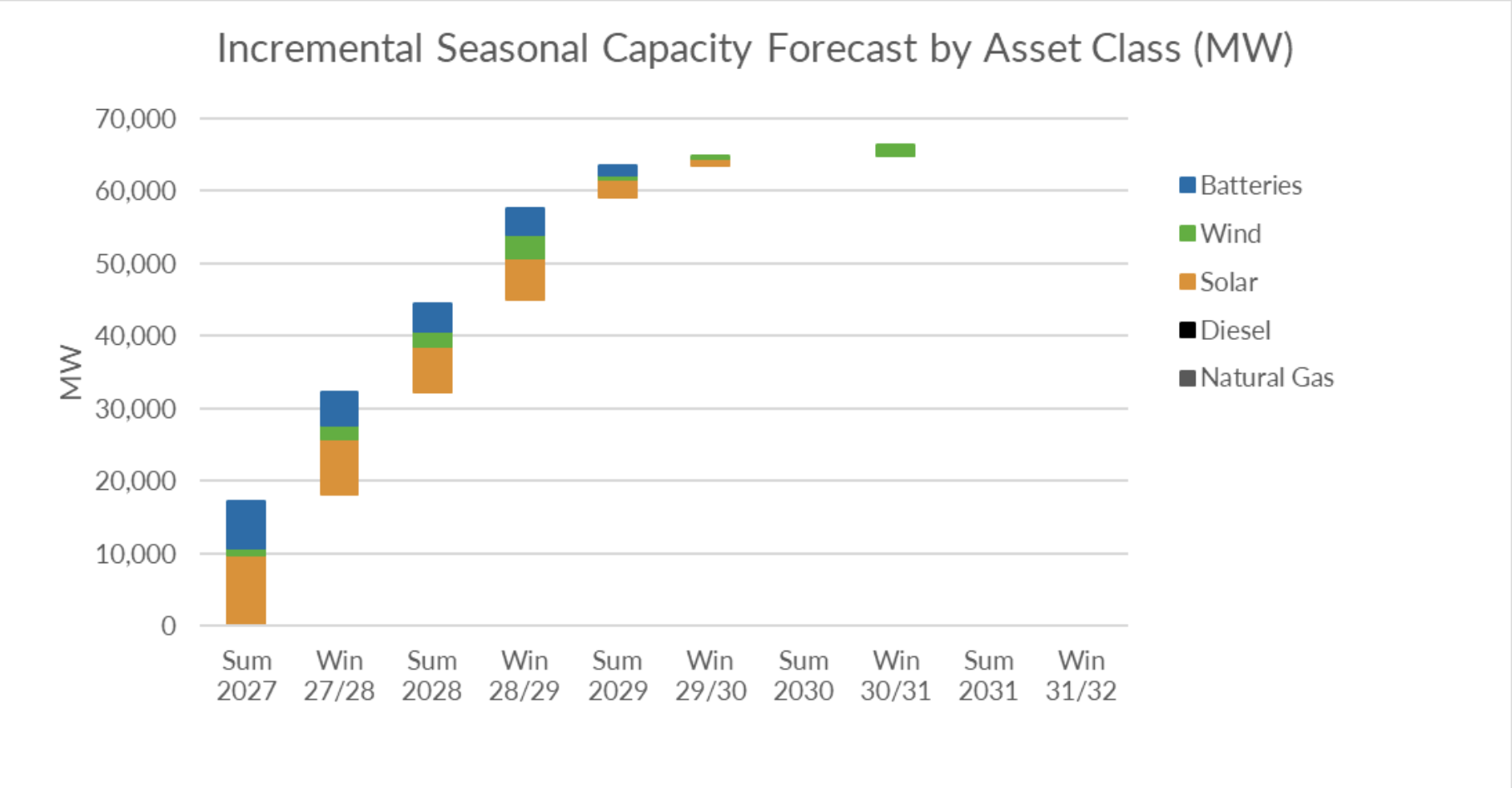

Despite the waiver request, ERCOT has published five-year summer and winter generation capacity projections, showing summer resource capacity growing from 185.7 GW in 2027 to 233.4 GW by 2031 and winter resource capacity growing from 204.4 GW in 2027/2028 to 237.2 GW by 2031/2032. Incremental generation capacity is expected to grow by more than 18 GW by Summer 2027 with solar providing over half the capacity, and batteries providing another 36% of the increased capacity. Renewables & batteries combined provide 95% of expected capacity growth through Winter 31/32, with solar providing 32.7GW, wind providing 10.8GW, and batteries providing 19.85GW. There is an expected 3.1GW of natural gas also expected between now and Winter 31/32. This forecast only represents those assets that have:

1) Achieved a fully executed Standard Generation Interconnection Agreement (SGIA) or a formal public commitment if it is a municipally owned utility;

2) Proof that the Interconnecting Entity (IE) has provided notice to proceed with the construction of interconnection facilities;

3) Provided the Transmission Service Provider (TSP) with sufficient financial security to fund the facility construction.