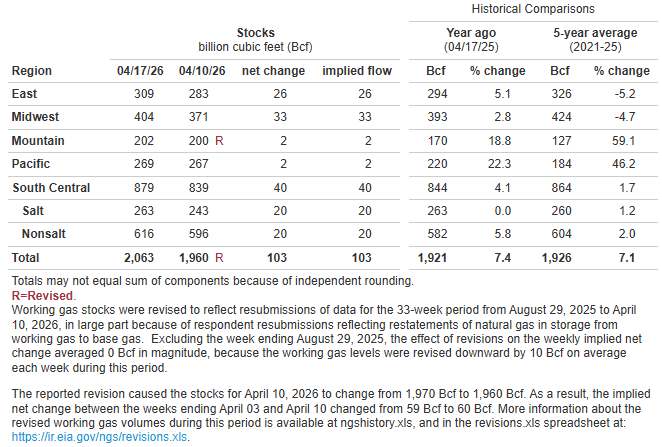

EIA Natural Gas Storage as of 4/17/26, as reported 4/23/26

*Working gas in storage was 2,063 Bcf as of Friday, April 17, 2026, according to EIA estimates. This represents a net increase of 103 Bcf from the previous week. Stocks were 142 Bcf higher than last year at this time and 137 Bcf above the five-year average of 1,926 Bcf. At 2,063 Bcf, total working gas is within the five-year historical range.

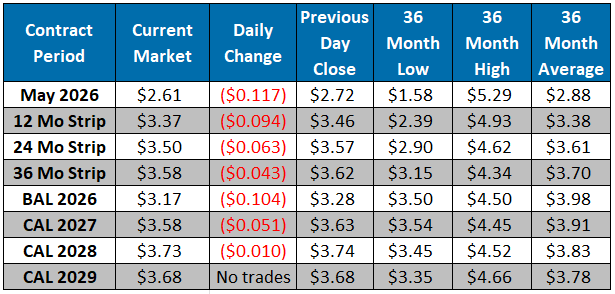

The NYMEX May contract closed at $2.72/MMBtu yesterday, a $0.03/MMBtu increase from Tuesday’s close. This week, May has averaged $2.70/MMBtu, around $0.07/MMBtu above last week’s average of $2.63/MMBtu. It is trading at $2.61/MMBtu, down $0.11/MMBtu from yesterday’s close. Supply has continued to ease through April, with production averaging ~109.5 Bcf/d for the month vs. ~111 Bcf/d prints early on – declines concentrated in the Northeast, Midcon, and non-Permian Texas, where weaker regional pricing is biting. EQT reinforced the theme on its earnings call, citing “tactical curtailments” in the Marcellus during shoulder season and flagging the potential for larger fall shut-ins if contango supports it. On the demand side, ResComm load remains suppressed as warmer-than-normal weather across the eastern US has pushed 30-day heating demand ~3 Bcf/d below year-ago levels, and weather models have continued to shed HDDs across the 1-15-day window. LNG feedgas is a bright spot at ~20 Bcf/d on the week, with Golden Pass shipping its inaugural cargo and Train 2 targeting late-summer startup. Longer term, China’s retreat from the spot LNG market to COVID-era import lows – reselling cargoes into elevated Iran-war pricing and leaning on Russian/Central Asian pipeline supply – is a caution flag for the demand-growth assumptions underpinning the back of the curve.

*Source: U.S. Energy Information Administration (EIA) Weekly Natural Gas Storage Report

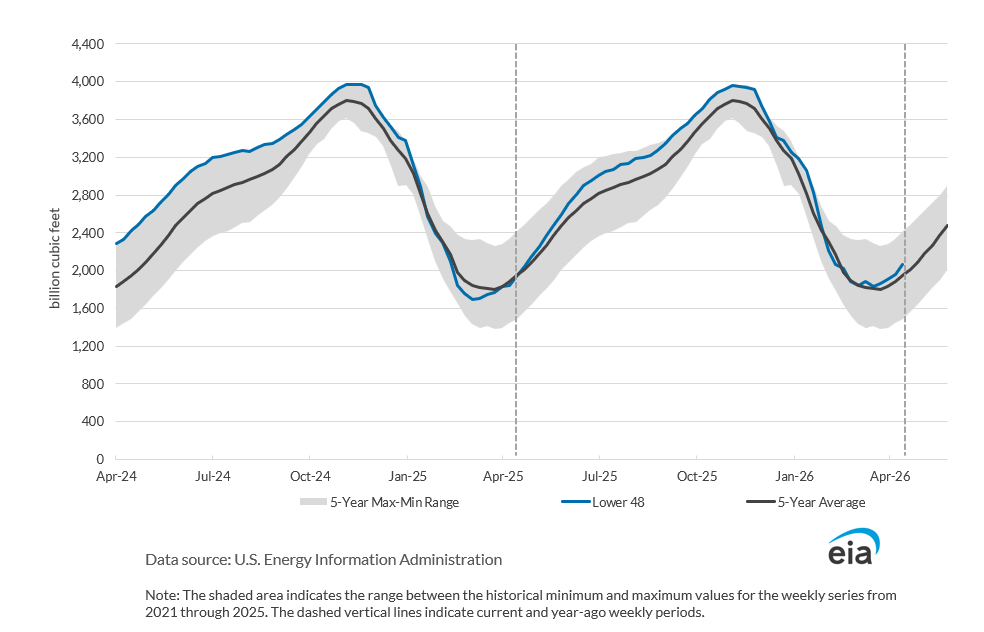

Working Gas in Underground Storage, Lower 48

Working Gas in Underground Storage vs. 5-Year Maximum and Minimum

Current Market