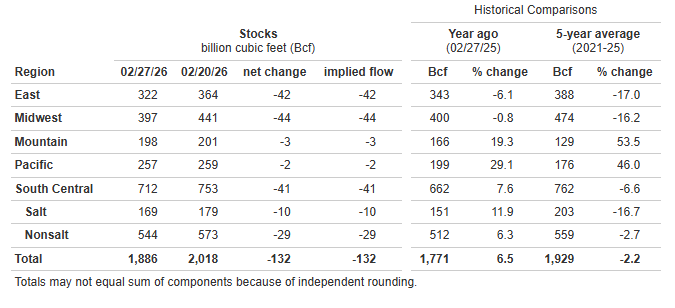

EIA Natural Gas Storage as of 2/27/26, as reported 3/5/26

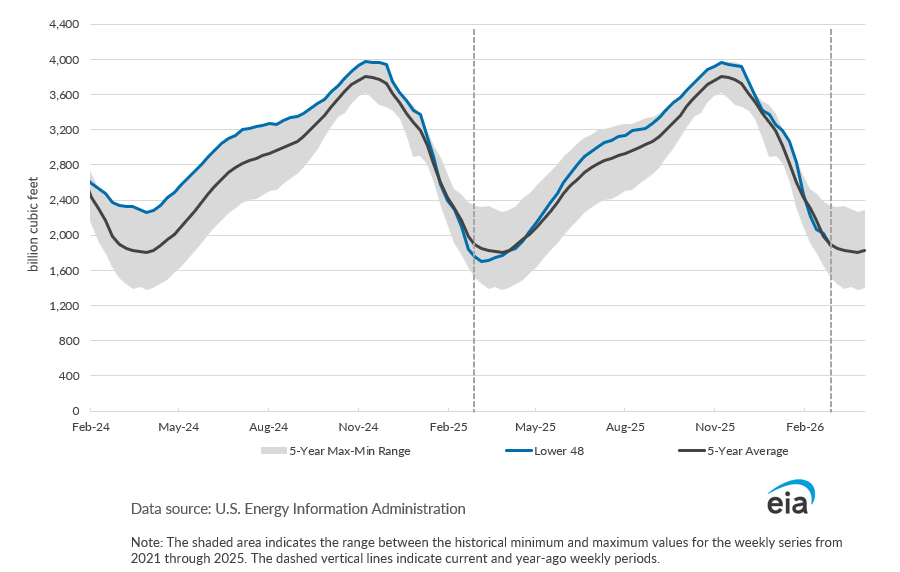

*Working gas in storage was 1,886 Bcf as of Friday, February 27, 2026, according to EIA estimates. This represents a net decrease of 132 Bcf from the previous week. Stocks were 115 Bcf higher than last year at this time and 43 Bcf below the five-year average of 1,929 Bcf. At 1,886 Bcf, total working gas is within the five-year historical range.

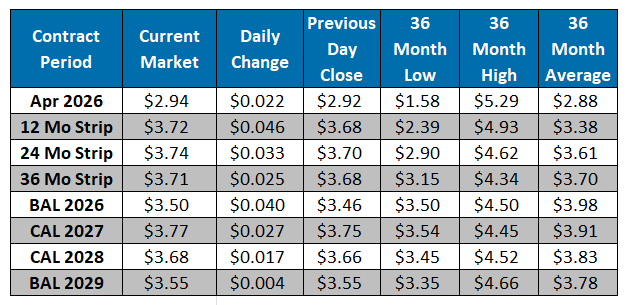

The NYMEX April contract closed at $2.92/MMBtu yesterday, a $0.14/MMBtu increase from Tuesday’s close. This week, April has averaged $2.97/MMBtu, around $0.11/MMBtu above last week’s average of $2.86/MMBtu. It is trading at $2.94/MMBtu, up $0.02/MMBtu from the previous day’s close. Natural gas prices remain near recent lows as warmer weather continues to erode late-season heating demand across key consuming regions L48 production remains strong near 109-110 Bcf/d, with NE output holding above 36 Bcf/d following recent gains, reinforcing a well-supplied backdrop even as Permian volumes ease modestly from earlier highs. Forecast revisions continue to trim heating demand expectations, with much of the country trending warmer through the near-term outlook before a potential cooler shift develops later in the extended window. LNG feedgas nominations remain solid near 19 Bcf/d, though short-term maintenance at Sabine Pass and weaker flows to Golden Pass have created modest variability in export demand. Mexican exports remain steady near 6.5 Bcf/d, while Canadian imports have fallen as mild temperatures reduce heating needs across the NE and MW. ResComm demand is expected to decline further into early next week as warmer conditions persist across the eastern half of the country.

*Source: U.S. Energy Information Administration (EIA) Weekly Natural Gas Storage Report

Working Gas in Underground Storage, Lower 48

Working Gas in Underground Storage vs. 5-Year Maximum and Minimum

Current Market