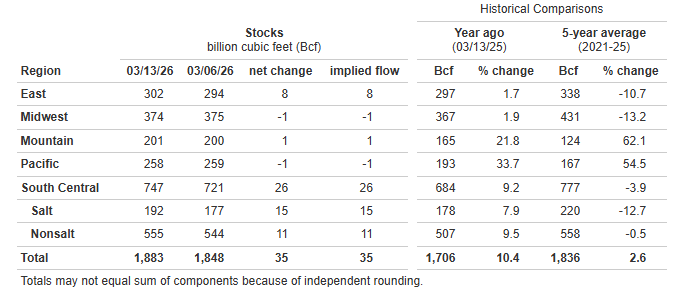

EIA Natural Gas Storage as of 3/13/26, as reported 3/19/26

*Working gas in storage was 1,883 Bcf as of Friday, March 13, 2026, according to EIA estimates. This represents a net increase of 35 Bcf from the previous week. Stocks were 177 Bcf higher than last year at this time and 47 Bcf above the five-year average of 1,836 Bcf. At 1,883 Bcf, total working gas is within the five-year historical range.

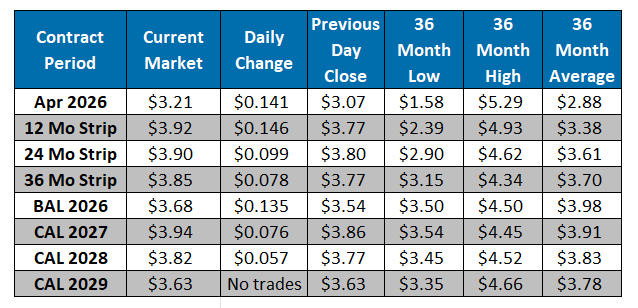

The NYMEX April contract closed at $3.07/MMBtu yesterday, a $0.03/MMBtu increase from Tuesday’s close. This week, April has averaged $3.08/MMBtu, around $0.06/MMBtu below last week’s average of $3.14/MMBtu. It is trading at $3.21/MMBtu, up $0.14/MMBtu from the previous day’s close. Natural gas prices have moved higher in recent sessions as escalating geopolitical tensions in the Middle East, particularly disruptions to Qatari LNG infrastructure, continue to support the broader energy complex. Despite this strength, underlying domestic fundamentals remain relatively soft. L48 production is trending higher near 109-110 Bcf/d, with gains across the NE and Permian reinforcing a well-supplied backdrop even as demand weakens. LNG feedgas nominations remain strong near 19.8 Bcf/d, with flows to Sabine rebounding following recent maintenance, while Mexican exports hold steady near 6.3 Bcf/d. Canadian imports have declined as milder weather reduces heating demand across key consuming regions. ResComm demand has dropped sharply, down roughly 25% DoD, as temperatures moderate across the East and MW, though a brief return of colder conditions next week may provide temporary support. While short-term price action is being driven by global LNG disruptions and broader energy market strength, weather guidance continues to trend mixed to warmer overall, and the market is entering the early stages of injection season.

*Source: U.S. Energy Information Administration (EIA) Weekly Natural Gas Storage Report

Working Gas in Underground Storage, Lower 48

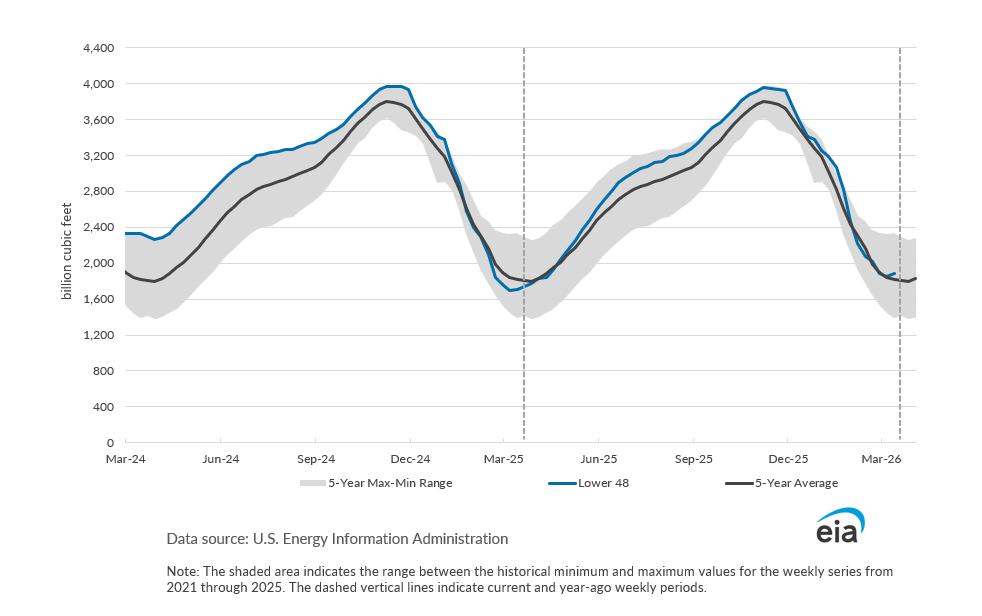

Working Gas in Underground Storage vs. 5-Year Maximum and Minimum

Current Market