EIA Natural Gas Storage as of 1/30/26, as reported 2/5/26

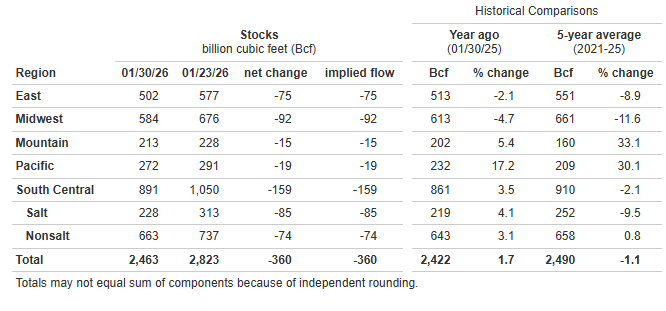

*Working gas in storage was 2,463 Bcf as of Friday, January 30, 2026, according to EIA estimates. This represents a net decrease of 360 Bcf from the previous week. Stocks were 41 Bcf higher than last year at this time and 27 Bcf below the five-year average of 2,490 Bcf. At 2,463 Bcf, total working gas is within the five-year historical range.

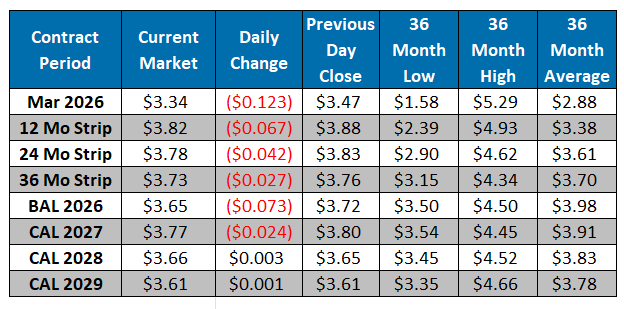

The NYMEX March contract closed at $3.47/MMBtu yesterday, a $0.15/MMBtu increase from Tuesday’s close. This week, March has averaged $3.34/MMBtu, around $0.61/MMBtu below last week’s average of $3.94/MMBtu. It is trading at $3.34/MMBtu, down $0.12/MMBtu from the previous day’s close. Natural gas prices moved higher in recent sessions as strong cash markets helped pull futures upward, though gains moderated as production continued to recover following January freeze-offs. L48 output has rebounded to roughly 108 Bcf/d, with NE volumes improving and Haynesville production now exceeding pre-freeze levels, supporting expectations that overall supply returns to 109-110 Bcf/d by mid-February. LNG feedgas nominations remain robust near 19.3-19.5 Bcf/d, with flows largely normalized across the complex despite a modest DoD dip at Freeport that has not been accompanied by a decline in power burn. ResComm demand is little changed DoD, as stronger heating demand in the NE is offset by weaker conditions in the MW and South, though demand in the NE is expected to strengthen over the weekend before easing later next week. Canadian imports remain elevated, averaging ~7.7 Bcf/d over the past week, while Mexican exports continue to firm near 6-6.5 Bcf/d, reinforcing a near-term balance that remains tight even as supply recovery begins to cap sustained upside.

*Source: U.S. Energy Information Administration (EIA) Weekly Natural Gas Storage Report

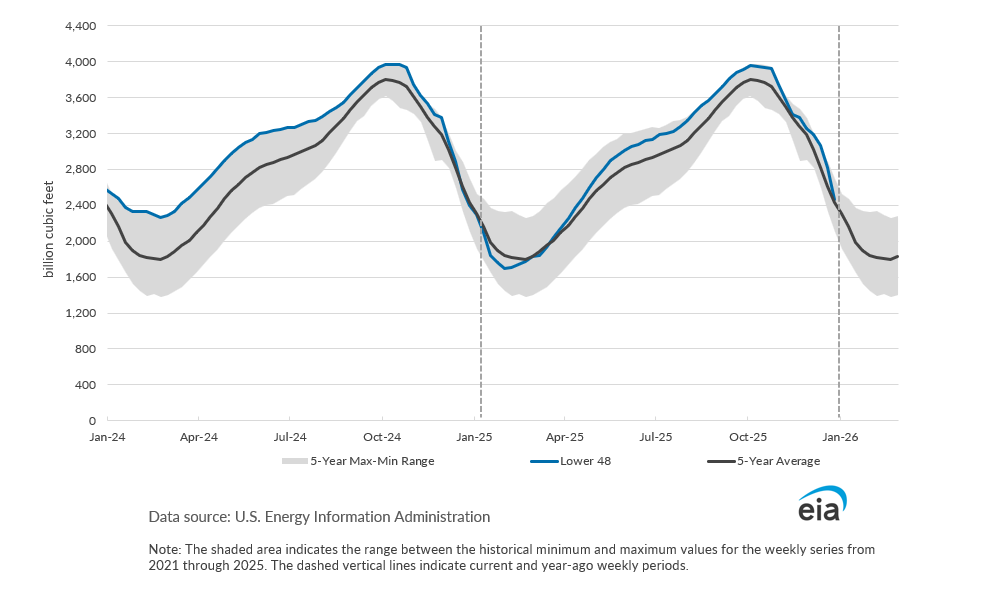

Working Gas in Underground Storage, Lower 48

Working Gas in Underground Storage vs. 5-Year Maximum and Minimum

Current Market