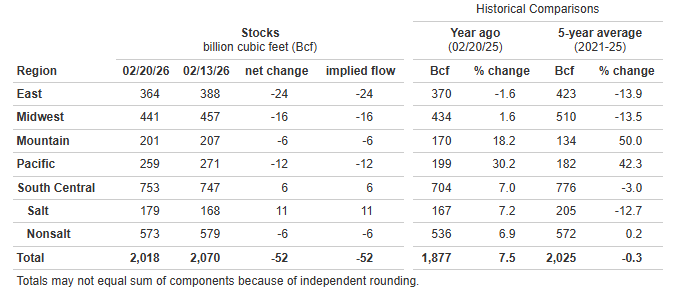

EIA Natural Gas Storage as of 2/20/26, as reported 2/26/26

*Working gas in storage was 2,018 Bcf as of Friday, February 20, 2026, according to EIA estimates. This represents a net decrease of 52 Bcf from the previous week. Stocks were 141 Bcf higher than last year at this time and 7 Bcf below the five-year average of 2,025 Bcf. At 2,018 Bcf, total working gas is within the five-year historical range.

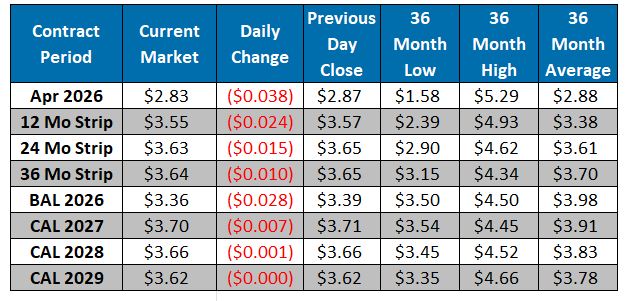

The March contract expired yesterday and settled at $2.97/MMBtu. The NYMEX April contract closed at $2.87/MMBtu yesterday, a $0.04/MMBtu increase from Tuesday’s close. This week, April has averaged $2.86/MMBtu, around $0.12/MMBtu below last week’s average of $2.98/MMBtu. It is trading at $2.83/MMBtu, down $0.04/MMBtu from the previous day’s close. Natural gas prices are breaking lower as aggressive HDD losses and a rapidly warming March outlook weigh on late-season demand expectations. L48 production remains resilient near 108-108.5 Bcf/d, with NE output climbing back toward 36 Bcf/d even as Permian volumes ease from earlier highs, reinforcing a fundamentally well-supplied backdrop. LNG feedgas nominations continue to run strong near 19.8 Bcf/d, with Golden Pass advancing toward initial liquefication after recent FERC approvals, while Mexican exports hold near 6 Bcf/d and Canadian imports remain modest. ResComm demand is softening as temperatures moderate across much of the East and MW and extended-range guidance continues to trend warmer across key consuming regions. With production steady and weather turning less supportive, the market appears increasingly focused on the seasonal shift toward injection dynamics and a softer early-spring demand profile.

*Source: U.S. Energy Information Administration (EIA) Weekly Natural Gas Storage Report

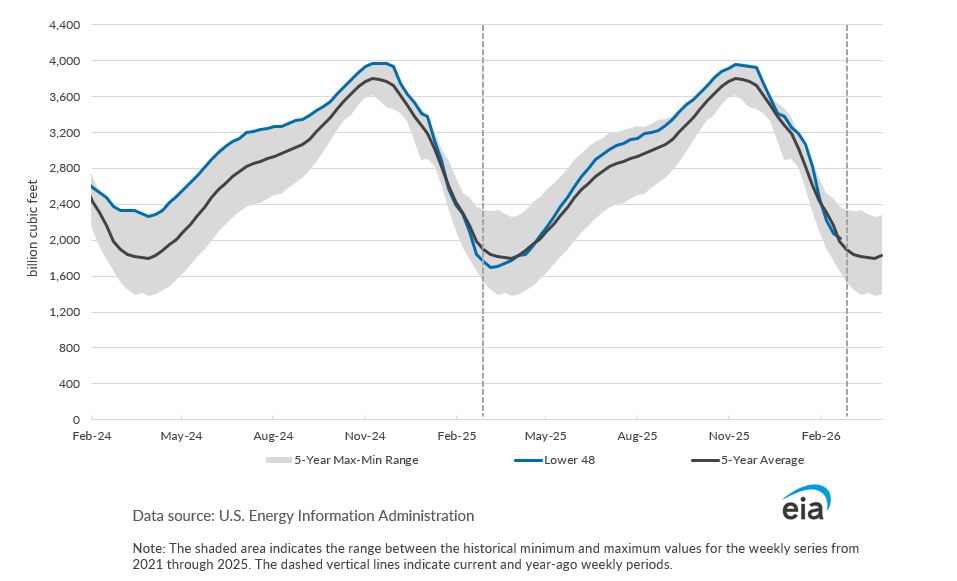

Working Gas in Underground Storage, Lower 48

Working Gas in Underground Storage vs. 5-Year Maximum and Minimum

Current Market