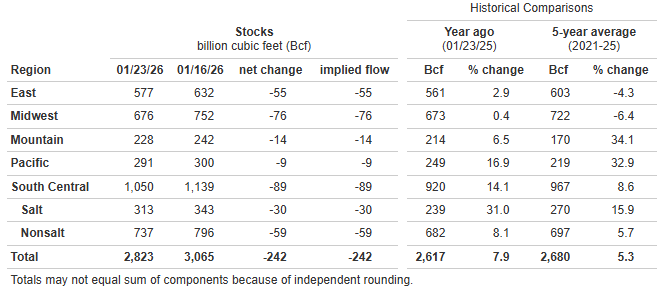

EIA Natural Gas Storage as of 1/23/26, as reported 1/29/26

*Working gas in storage was 2,823 Bcf as of Friday, January 23, 2026, according to EIA estimates. This represents a net decrease of 242 Bcf from the previous week. Stocks were 206 Bcf higher than last year at this time and 143 Bcf above the five-year average of 2,680 Bcf. At 2,823 Bcf, total working gas is within the five-year historical range.

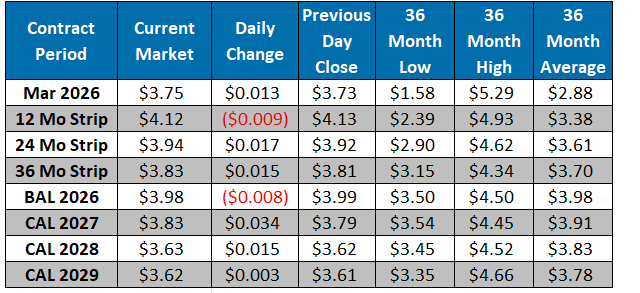

The February contract expired yesterday and settled at $7.46/MMBtu. The NYMEX March contract closed at $3.73/MMBtu yesterday, a $0.08/MMBtu decrease from Tuesday’s close. This week, March has averaged $3.80/MMBtu, around $0.47/MMBtu above last week’s average of $3.33/MMBtu. It is trading at $3.75/MMBtu, up $0.01/MMBtu from the previous day’s close.Natural gas prices remain volatile as freeze-offs impacts ease across much of the southern U.S., allowing production to rebound while cold-driven demand stays elevated across key consuming regions. L48 output has recovered to roughly 103-104 Bcf/d, with remaining freeze-offs estimated near 6 Bcf, though renewed sub-freezing temperatures moving into the Permian and Haynesville this weekend could trigger additional short-term disruptions. LNG feedgas nominations have strengthened to ~19.5 Bcf/d, with most facilities back online aside from Elba, and expectations building for initial liquefication at Golden Pass by early March following recent regulatory approvals. ResComm demand has softened modestly on milder weather in the South but is expected to rebound into the weekend as colder temperatures spread into the South Central, while demand across the East and MW remain well above seasonal norms and should persist for at least two weeks.

*Source: U.S. Energy Information Administration (EIA) Weekly Natural Gas Storage Report

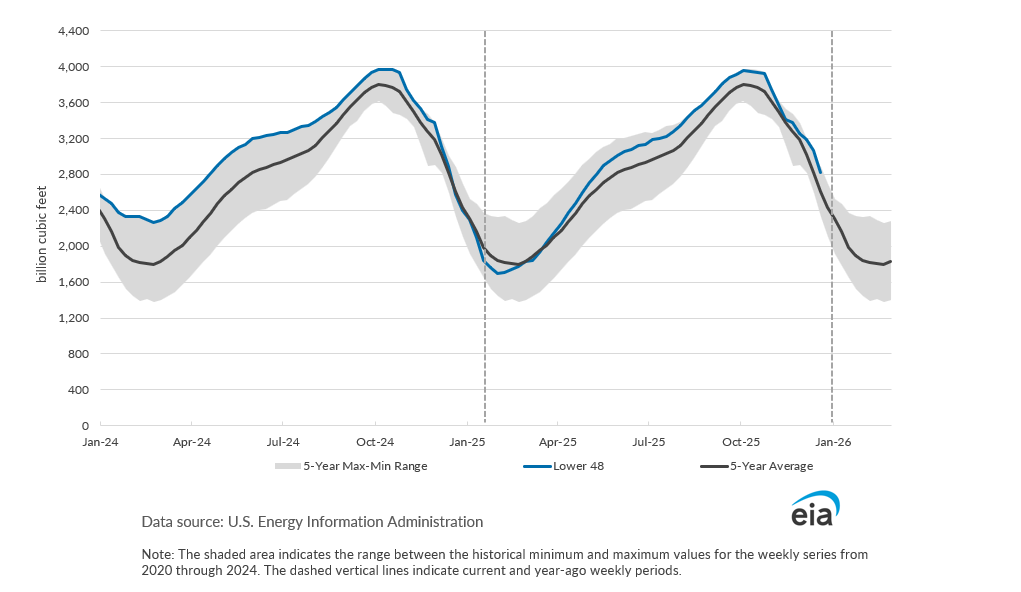

Working Gas in Underground Storage, Lower 48

Working Gas in Underground Storage vs. 5-Year Maximum and Minimum

Current Market