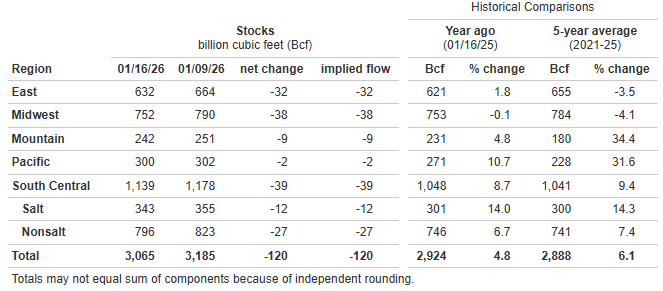

EIA Natural Gas Storage as of 1/16/26, as reported 1/22/26

*Working gas in storage was 3,065 Bcf as of Friday, January 16, 2026, according to EIA estimates. This represents a net decrease of 120 Bcf from the previous week. Stocks were 141 Bcf higher than last year at this time and 177 Bcf above the five-year average of 2,888 Bcf. At 3,065 Bcf, total working gas is above the five-year historical range.

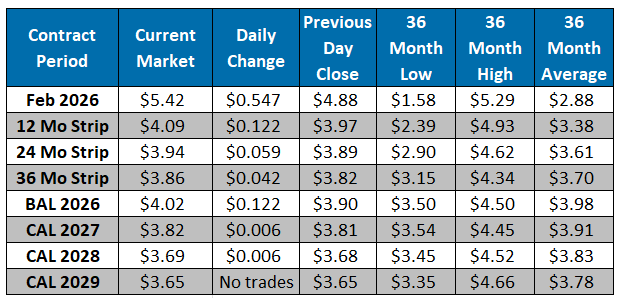

The NYMEX February contract closed at $4.88/MMBtu yesterday, a $0.97/MMBtu increase from Tuesday’s close. This week, February has averaged $4.72/MMBtu, around $1.48/MMBtu above last week’s average of $3.24/MMBtu. It is trading at $5.42/MMBtu, up $0.55/MMBtu from the previous day’s close as short covering and an intensifying Arctic blast drive historic volatility. This rally is fueled by weather models aligning on extreme cold, with the GFS adding 16 HDDs to match the bullish Euro model, while Chicago wind chills are expected to reach -35°F. Production, which was recently revised to 107.3 Bcf/d, is facing severe risk as freeze-offs are expected to peak between January 24–26 across the Permian, Texas, Oklahoma, and the Haynesville, with SpringRock estimating potential losses exceeding 100 Bcf over the next two weeks. In response, heating demand is projected to rise sharply, with Storage Week 2 demand forecasted at 98.5 Bcf/day—up 27.5 Bcf/day year-over-year—as arctic air dominates the eastern half of the U.S. into early February. Consequently, physical hub cash is shaping up to trade around $6/MMBtu while Canadian imports and storage withdrawals accelerate, pushing the projected end-of-March storage down to 1,650 Bcf.

*Source: U.S. Energy Information Administration (EIA) Weekly Natural Gas Storage Report

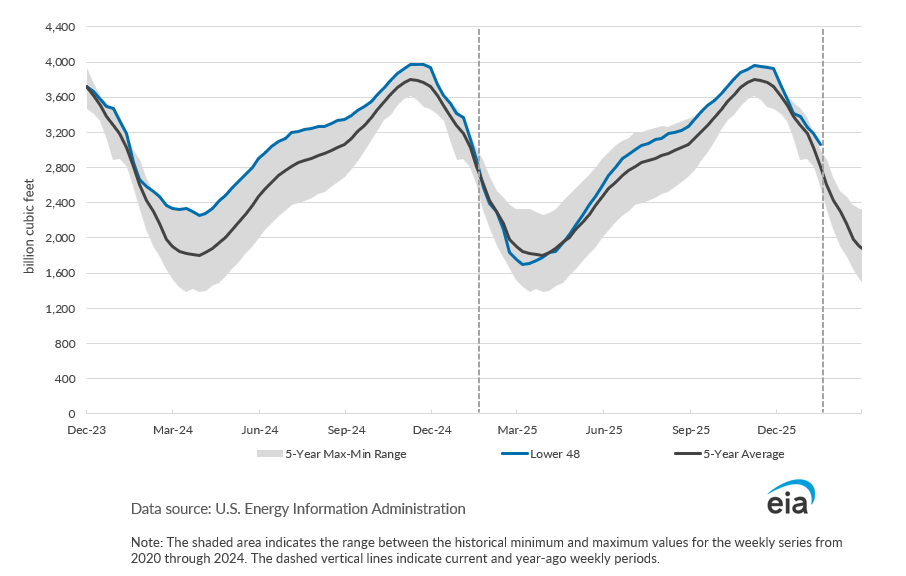

Working Gas in Underground Storage, Lower 48

Working Gas in Underground Storage vs. 5-Year Maximum and Minimum

Current Market