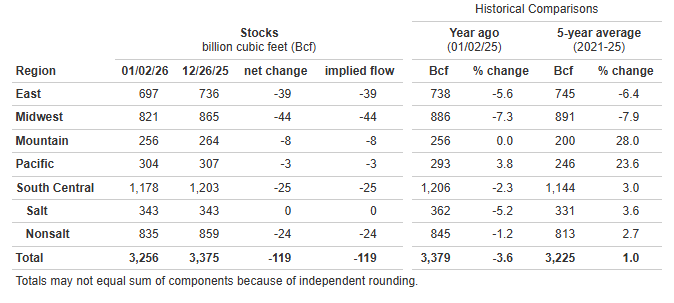

EIA Natural Gas Storage as of 1/2/26, as reported 1/8/26

*Working gas in storage was 3,256 Bcf as of Friday, January 2, 2026, according to EIA estimates. This represents a net decrease of 119 Bcf from the previous week. Stocks were 123 Bcf less than last year at this time and 31 Bcf above the five-year average of 3,225 Bcf. At 3,256 Bcf, total working gas is within the five-year historical range.

The NYMEX February contract closed at $3.52/MMBtu yesterday, a $0.18/MMBtu increase from Tuesday’s close. This week, February has averaged $3.45/MMBtu, around $0.32/MMBtu below last week’s average of $3.78/MMBtu. It is trading at $3.43/MMBtu, down $0.10/MMBtu from the previous day’s close. Natural gas prices moved lower despite additional cold being added to late-January forecasts, as the market continues to fade weather signals amid steady supply and lingering skepticism following recent forecast volatility. L48 production remains elevated near 109-110 Bcf/d, with intraday revisions lifting Permian and Marcellus output, though freeze-off risk is rising as colder air increasingly targets the NE later this month. LNG feedgas nominations have eased to ~19.4 Bcf/d, with modest gains at Sabine partially offsetting softer flows elsewhere, while Mexican exports remain firm near 6.4 Bcf/d and Canadian imports have averaged ~6.1 Bcf/d over the past week. Res/Comm demand is modestly higher DoD but remains below longer-term norms amid continued near-term warmth, with a transition toward sustained cold in the East and MW expected by mid-January.

*Source: U.S. Energy Information Administration (EIA) Weekly Natural Gas Storage Report

Working Gas in Underground Storage, Lower 48

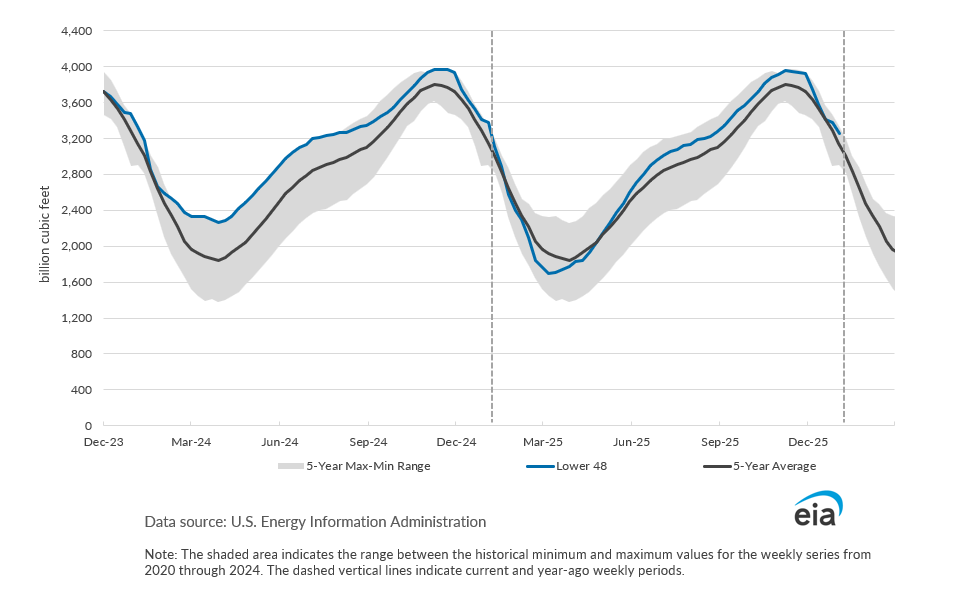

Working Gas in Underground Storage vs. 5-Year Maximum and Minimum

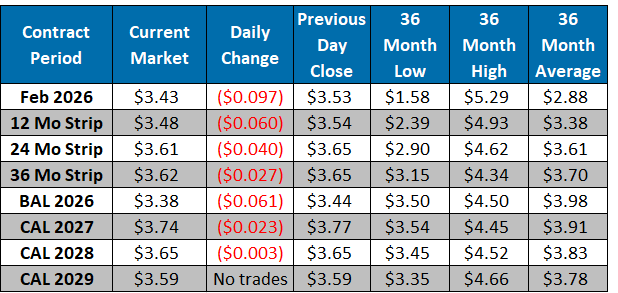

Current Market