The Inflation Reduction Act (IRA), which was signed into law by President Biden in August 2022, seeks to lower inflation, in one way, by supporting domestic energy production and promoting clean energy. This includes a significant expansion of tax credit qualifications for wind, solar, battery storage and other power generation technologies. For example, any zero greenhouse-gas-emitting power generating facilities beginning construction after 2024 are eligible for either a new Production Tax Credit (PTC) or an Investment Tax Credit (ITC) through calendar year 2032 with potential phaseouts thereafter, while existing tax credit status has been extended to any projects beginning construction before January 1, 2025. Additionally, the Inflation Reduction Act reinstates total tax credit values for wind and solar while providing additional tax breaks for other technologies, including standalone battery storage, qualified biogas facilities and microgrid controller equipment. All these changes provide renewable developers the ability to expand over the next decade with significantly greater certainty of the achievable tax benefits regardless of construction start or COD date.

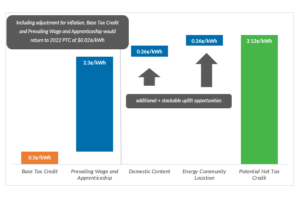

Regarding the Production Tax Credit, specifically, the IRA decreased the PTC to $0.003/kWh with a path to return the PTC to the full $0.015/kWh. Which with the current inflation adjustment brings the PTC to the current rate of $0.026/kWh for 2022. Projects meeting prevailing wage and apprenticeship requirements would achieve a 5X multiplier, returning the PTC to the full $0.015/kWh. Additionally, there is a potential for significant gain for wind projects given the removal of the phaseout reduction and the available additional uplifts (10% each if they meet the domestic content and energy community location requirements). Also Prior to the IRA, only wind projects post-2007 were eligible for the PTC, but now it’s available for solar projects as well.

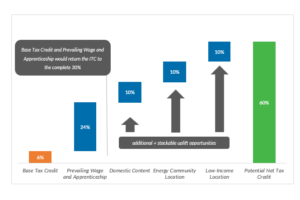

Solar and battery storage development is poised to expand further given the increase in tax credits, standalone Investment Tax Credit for battery storage, flexibility in PTC/ITC election, and the overall removal of ambiguity regarding future tax credit revenues. The IRA decreases the base ITC to 6% (previously 30% before step downs) with the path to 30% and a potential bonus of up to an additional 30% for qualifying projects. Both solar and standalone battery storage projects meeting prevailing wage and apprenticeship requirements would achieve a 5X multiplier, returning the ITC to the full 30%, with no step down until after Cal 2032 and, also, can receive additional ITC uplifts of 10% each (stackable) by meeting the requirements for domestic content, energy community location and low-income location. Further, solar projects can now claim either the ITC or PTC, whichever the developer prefers.

Solar and battery storage development is poised to expand further given the increase in tax credits, standalone Investment Tax Credit for battery storage, flexibility in PTC/ITC election, and the overall removal of ambiguity regarding future tax credit revenues. The IRA decreases the base ITC to 6% (previously 30% before step downs) with the path to 30% and a potential bonus of up to an additional 30% for qualifying projects. Both solar and standalone battery storage projects meeting prevailing wage and apprenticeship requirements would achieve a 5X multiplier, returning the ITC to the full 30%, with no step down until after Cal 2032 and, also, can receive additional ITC uplifts of 10% each (stackable) by meeting the requirements for domestic content, energy community location and low-income location. Further, solar projects can now claim either the ITC or PTC, whichever the developer prefers.

To fully support the U.S. initiative of moving away from fossil fuels, a myriad of subsidies and incentives have been added and/or extended through the IRA. Knowing that fossil fuels still make up a large percentage of the energy consumed, this transition away from those fossil fuels will be gradual. These changes include:

To fully support the U.S. initiative of moving away from fossil fuels, a myriad of subsidies and incentives have been added and/or extended through the IRA. Knowing that fossil fuels still make up a large percentage of the energy consumed, this transition away from those fossil fuels will be gradual. These changes include:

- Extends and expands 45Q (carbon capture) production tax credits

- Provides for construction starts as late as 2033

- Lowered minimum carbon capture requirement

- Increased to $85/mt for permanent storage and $60/mt for EOR

- Direct Air Capture (DAC) CO2 projects receive $180/mt for permanent, while CO2 EOR will receive $130/mt

- PTC for hydrogen facilities with prevailing wage and apprenticeship requirements and option for ITC rather than PTC

- PTC for nuclear facilities prior to enactment with prevailing wage and apprenticeship requirements

- Electric Vehicle (EV) charging station tax credit qualification extended until 2033 and includes similar prevailing wage and apprenticeship requirements as ITC

- EV tax credit of $7,500 with specifics on sourcing of components, price, and taxpayer income that can reduce the total credit

- Investment Tax Credits can now be transferred for cash to unrelated entities, which eliminates the complex tax equity structures previously employed

- Offshore oil and gas royalty rates have increased to a minimum of 16.66% and a maximum of 18.75%, up from 12.5%, while the minimum bid was also increased 5X to $10/acre

- Flared natural gas on federal lands will now receive royalties, where previously royalties were only available on sold natural gas

- Components essential to an energy transition away from fossil fuels now have incentives to support advanced mining and manufacturing to enable a substantially U.S.-maintained supply chain