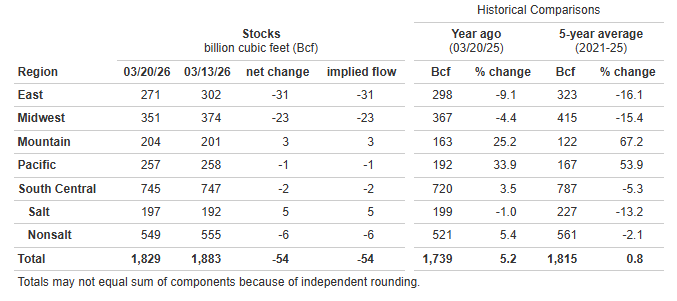

EIA Natural Gas Storage as of 3/20/26, as reported 3/26/26

*Working gas in storage was 1,829 Bcf as of Friday, March 20, 2026, according to EIA estimates. This represents a net decrease of 54 Bcf from the previous week. Stocks were 90 Bcf higher than last year at this time and 14 Bcf above the five-year average of 1,815 Bcf. At 1,829 Bcf, total working gas is within the five-year historical range.

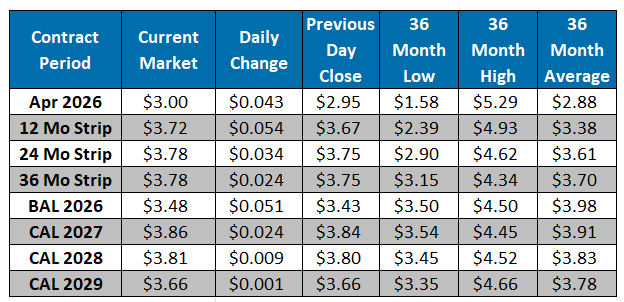

The NYMEX April contract closed at $2.95/MMBtu yesterday, a $0.01/MMBtu increase from Tuesday’s close. This week, April has averaged $2.94/MMBtu, around $0.13/MMBtu below last week’s average of $3.08/MMBtu. It is trading at $3.00/MMBtu, up $0.04/MMBtu from the previous day’s close. Natural gas prices remain under pressure as the market transitions into injection season, with warmer weather continuing to erode late-season heating demand across key consuming regions. L48 production remains strong near 109-110 Bcf/d, with recent gains in the Permian and Haynesville reinforcing a well-supplied backdrop. Forecast revisions continue to trend warmer overall, keeping ResComm demand subdued despite a brief cold shot expected over the weekend. LNG feedgas nominations have strengthened to ~20 Bcf/d, supported by the anticipated start-up of Train 5, while Mexican exports remain steady near 6.5 Bcf/d and Canadian imports have declined on weaker demand. With storage now essentially in line with five-year levels and injections expected to begin imminently, the market appears increasingly focused on shoulder-season fundamentals, where steady supply and soft demand continue to point to a relatively loose balance.

*Source: U.S. Energy Information Administration (EIA) Weekly Natural Gas Storage Report

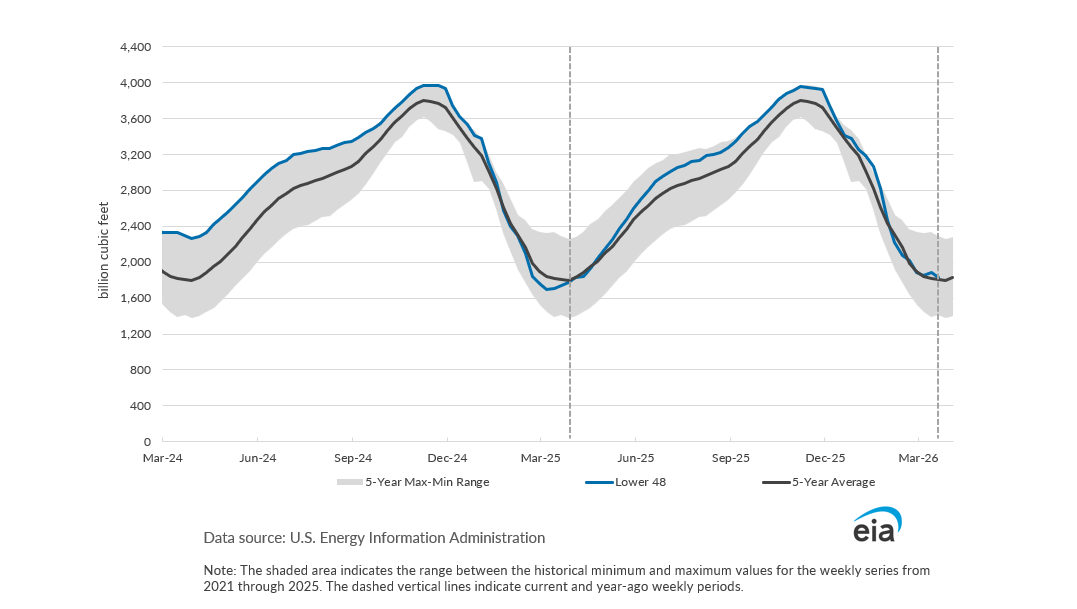

Working Gas in Underground Storage, Lower 48

Working Gas in Underground Storage vs. 5-Year Maximum and Minimum

Current Market