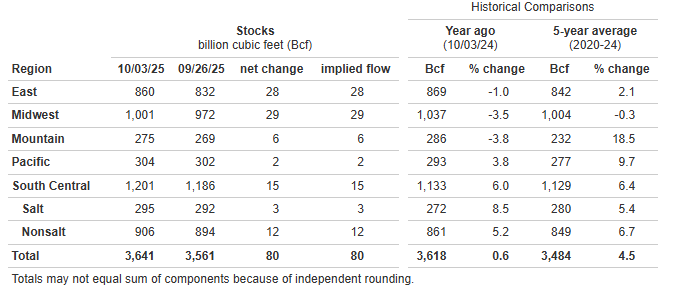

EIA Natural Gas Storage as of 10/3/25, as reported 10/9/25

* Working gas in storage was 3,641 Bcf as of Friday, October 3, 2025, according to EIA estimates. This represents a net increase of 80 Bcf from the previous week. Stocks were 23 Bcf higher than last year at this time and 157 Bcf above the five-year average of 3,484 Bcf. At 3,641 Bcf, total working gas is within the five-year historical range.

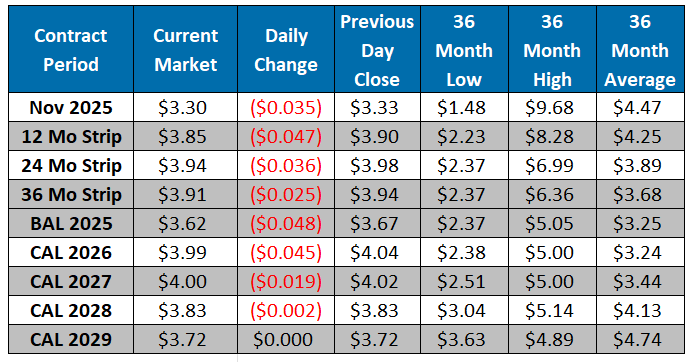

The NYMEX November contract closed at $3.33/MMBtu yesterday, a $0.11/MMBtu decrease from Tuesday’s close. This week, November has averaged $3.37/MMBtu, around $0.01/MMBtu above last week’s average of $3.36/MMBtu. It is trading at $3.30/MMBtu, down $0.04/MMBtu from the previous day’s close. Natural gas prices softened following today’s EIA storage report, which revealed an 80 Bcf injection, modestly above expectations in the 75-77 Bcf range. Supply-side fundamentals remain the key market driver, with L48 production revised higher to 105.5 Bcf/d yesterday on strong intraday revisions in the Permian and NE. Output has eased from last week’s highs but remains near record territory, and production is expected to stay elevated through the remainder of October. Cooler weather across the East and MW has weighed on power burns, which are down nearly 10% WoW, while increased wind generation in the South Central further curbed gas demand. LNG feedgas nominations are steady near 16.2 Bcf/d, and Cove Point maintenance is expected to wrap up within the next few days, adding back roughly 0.8 Bcf/d of flows. While today’s larger than expected build reinforces a comfortable storage position heading into winter, record supply and soft weather driven demand continue to limit any sustained upward momentum in prices.

*Source: U.S. Energy Information Administration (EIA) Weekly Natural Gas Storage Report

Working Gas in Underground Storage, Lower 48

Working Gas in Underground Storage vs. 5-Year Maximum and Minimum

Current Market